The real question behind the

prime minister's fibs at his party conference, just like last year's fibs by the

chancellor of the exchequer, is this: why does the Labour Party let the Tories define the narrative?

Last year Mr Osborne's fibs were in the service of creating a version of history in which the crisis was caused by too much debt. (Respectable Keynesians might agree that the explosion of debt was a cause but it was mainly

household and businesses who were running up the debt.)

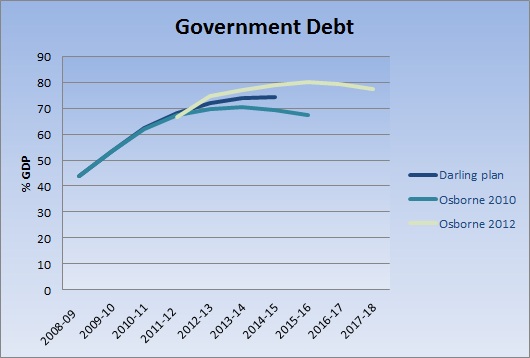

In Mr Osborne's version the borrowers were the British government, European governments and (bizarrely) the banks. This was and is nonsense. Before the crisis the government's net debt ratio was 36.4% of GDP. European countries which are now highly indebted include

Spain and Ireland who, before the crisis were paying down their national debt, which was already very low. The banks were culprits not because they

borrowed too much, but because they

lent too much.

Mr Cameron returns to the theme by painting Labour as inveterate borrowers.

This alternative history needs to be countered. The opposition must create a different narrative, and one which is more honest. Against the Tory story of a debt crisis which must be cured by austerity we need a narrative to explain that the problem is a financial collapse and the solution is investment.

Simple Keynesian analysis reminds us that the stimulus the economy needs is investment rather than general government spending or tax cuts. The investment may be in the public sector or the private sector or done by the public sector because the private sector is unwilling.

Investment should raise the potential of the economy and so provide more jobs and output in future and reduces the structural deficit. Investment should provide future income streams and so it is usual to fund investment by borrowing.

This is not the time to be slashing government investment in half, as

Jonathan Portes of NIESR argues.

|

| Source: Jonathan Portes blog, Not the Treasury View |

To boost private sector investment a future Labour government will need to fix the still broken financial sector to provide the economy with the kind of banks which supply credit to small and medium sized businesses. New lenders will be needed, such as regional enterprise banks, and barriers to entry for new retail banks should be removed.

These then should be the themes of a new narrative to explain the crisis and its resolution. They are easily understandable. People remember that the crisis began as a financial crisis, but perhaps need to be reminded of collateralised debt obligations, shadow banking, securitisation, special investment vehicles, sub-prime lending and all the other instruments of financial destruction. Investment too is an attractive concept which points to a brighter future.

A narrative is not yet a policy, but as I will argue, the policy should point in this direction.

Update: link added